There is nothing more frustrating than knowing you can afford a home, but having a bank tell you otherwise. I’ve seen it happen countless times: successful business owners, savvy real estate investors, or gig workers with solid income getting rejected simply because they don’t fit the rigid “9-to-5” box required by Fannie Mae or Freddie Mac.

If that sounds like your situation, you don’t need a new job. You need a Non-QM (Non-Qualified Mortgage) loan.

In this guide, I’ve analyzed the market to bring you the best Non-QM lenders for 2026. These companies specialize in looking at your real ability to pay, using bank statements or asset portfolios instead of just tax returns. Later on, I’ll also share a specific tool, Bluerate, that I recently tested to help you compare real-time rates and find qualified officers without the usual sales harassment.

5 Top Non-QM Mortgage Lenders

Finding a lender that understands the nuance of your income is critical. I have selected the following five companies based on their reputation, product flexibility, underwriting speed, and digital experience in 2026.

#1. First National Bank of America

Best for: Self-Employed Borrowers seeking stability.

Unlike many “shops” that just originate loans and sell them, First National Bank of America (FNBA) is a portfolio lender. This is a huge advantage. Because they hold the loans on their own books, they make their own rules. They have been in the “Non-Traditional” mortgage game for decades and have a reputation for funding deals that other banks won’t touch.

Key Features:

-

12-Month Bank Statements: Great for business owners.

-

ITIN Loans: Available for borrowers without a Social Security Number.

-

Recent Credit Events: They are more forgiving of past bankruptcies if you’ve re-established credit.

-

High LTV: Competitive Loan-to-Value ratios for qualified buyers.

#2. LendFriend Mortgage

Best for: First-Time Homebuyers wanting a digital-first experience.

If you hate paperwork and slow responses, LendFriend is a breath of fresh air. They position themselves as a modern, tech-forward lender. Their goal is to remove the friction from the mortgage process. In 2026, speed matters. LendFriend’s platform allows for quick uploads and faster processing times, which is crucial in a competitive housing market.

Key Features:

-

Fast Closing: Known for closing loans in weeks, not months.

-

User-Friendly Portal: Easy to track your loan status 24/7.

-

Purchase Focused: They specialize in helping buyers win offers.

-

Competitive Non-QM Rates: They aggressively price their alternative doc loans.

#3. CrossCountry Mortgage

Best for: Borrowers who need a wide variety of options.

CrossCountry Mortgage (CCM) is a giant in the industry. They are a top-tier retail lender with branches everywhere. While they do massive amounts of standard loans, their Non-QM division is surprisingly robust and flexible. They offer a “one-stop-shop” experience. If it turns out you don’t need a Non-QM loan, they can easily switch you to an FHA or Conventional loan without you having to change companies.

Key Features:

-

Asset Depletion Loans: qualifying based on your liquid assets.

-

Investor Cash Flow: Strong DSCR programs for landlords.

-

Hybrid Options: They have products that bridge the gap between Prime and Non-QM.

-

Local Expertise: Thousands of loan officers who know local markets well.

#4. Angel Oak Mortgage Solutions

Best for: Real Estate Investors and Complex Scenarios.

You can’t talk about Non-QM without mentioning Angel Oak. They are widely considered the leader and pioneer in the Non-QM space. They practically invented the modern version of these loans after the 2008 crash. They have seen every difficult scenario imaginable. If your financial situation is extremely complex (e.g., multiple businesses, foreign income), Angel Oak is often the go-to.

Key Features:

-

Bank Statement Loans: The industry standard for self-employed.

-

DSCR Loans: No income verification needed for investment properties.

-

Foreign National Programs: Excellent for non-US citizens buying here.

-

Jumbo Non-QM: Loans up to $3M+ for luxury properties.

#5. New American Funding

Best for: Underserved communities and Manual Underwriting.

New American Funding (NAF) has built a brand around inclusivity. They are excellent at “Manual Underwriting,” which means a human being reviews your file rather than a computer algorithm instantly rejecting you. They look at the “whole story.” If your credit score is low due to a life event (like a medical emergency) but your income is strong, NAF is willing to listen.

Key Features:

-

Manual Underwriting: Human review for tricky credit files.

-

Bilingual Support: Extensive support for Spanish-speaking borrowers.

-

Self-Employed Friendly: Strong programs for 1099 workers.

-

Custom Terms: Flexible loan terms to fit your budget.

Tip: Where to Find Non-QM Loan Officers?

Knowing the best lenders is only half the battle. The real challenge is finding a Loan Officer who actually understands Non-QM guidelines.

If you walk into a random bank branch, 9 out of 10 officers won’t know how to structure a Bank Statement loan. You could waste weeks sending documents to the wrong person.

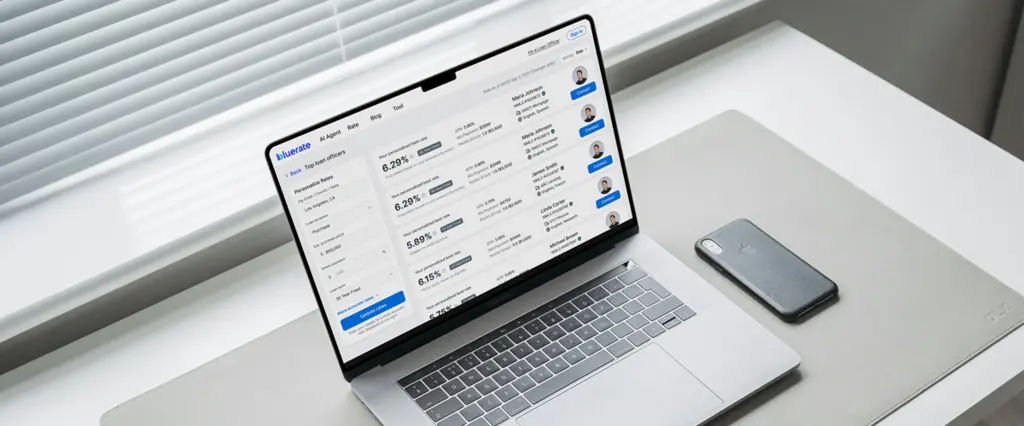

This is where a platform like Bluerate.ai becomes a game-changer.

I recently explored Bluerate, and it’s fundamentally different from those spammy “get a quote” sites. It is an AI-powered Mortgage Marketplace designed to modernize how we get loans.

Why I recommend using Bluerate:

-

Real Rates, No Teasers: Bluerate connects directly to the pricing engines of nearly 30 major lenders. The rate you see is based on live data, not a fake number just to get you to click.

-

You Pick the Officer: Instead of being randomly assigned to a call center, you can search for local Loan Officers. You can see their NMLS credentials, their experience, and their specialties. Bluerate vets these officers, ensuring you only deal with professionals who have a clean track record.

-

Zero Spam (Privacy First): This is my favorite part. They do not sell your data to lenders. You decide who to contact. You won’t get 50 robocalls the moment you hit “submit.”

-

AI-Powered Efficiency: You can input your info (Credit score, estimated purchase price, gross monthly income, etc.) to get a Personalized Rate instantly. If you are ready to move, you can even pre-qualify online.

-

Tech-Savvy: For those who know the industry, Bluerate allows you to export your data in FNM 3.4 format. It also automates the generation of the 1003 loan application form, minimizing errors and speeding up the process.

-

Secure & Free: The platform is SOC 2 Type II certified (enterprise-grade security) and completely free for borrowers.

It basically allows you to skip the middleman chaos and go straight to a vetted expert who knows how to handle your specific Non-QM needs.

Final Word

The mortgage landscape in 2026 is more flexible than ever before. Being self-employed or having a unique financial situation is no longer a barrier to homeownership. Lenders like First National Bank of America and Angel Oak have created incredible products to serve you.

However, the “Non-QM” world is complex. Rates and guidelines vary wildly between lenders.

My best advice? Don’t go it alone. Use a tool like Bluerate.ai to verify what the market rates actually look like for your scenario. Compare the numbers, find a vetted Loan Officer who specializes in self-employed or investor loans, and start a conversation. Your dream home is likely within reach. You just need the right team to help you close the deal.